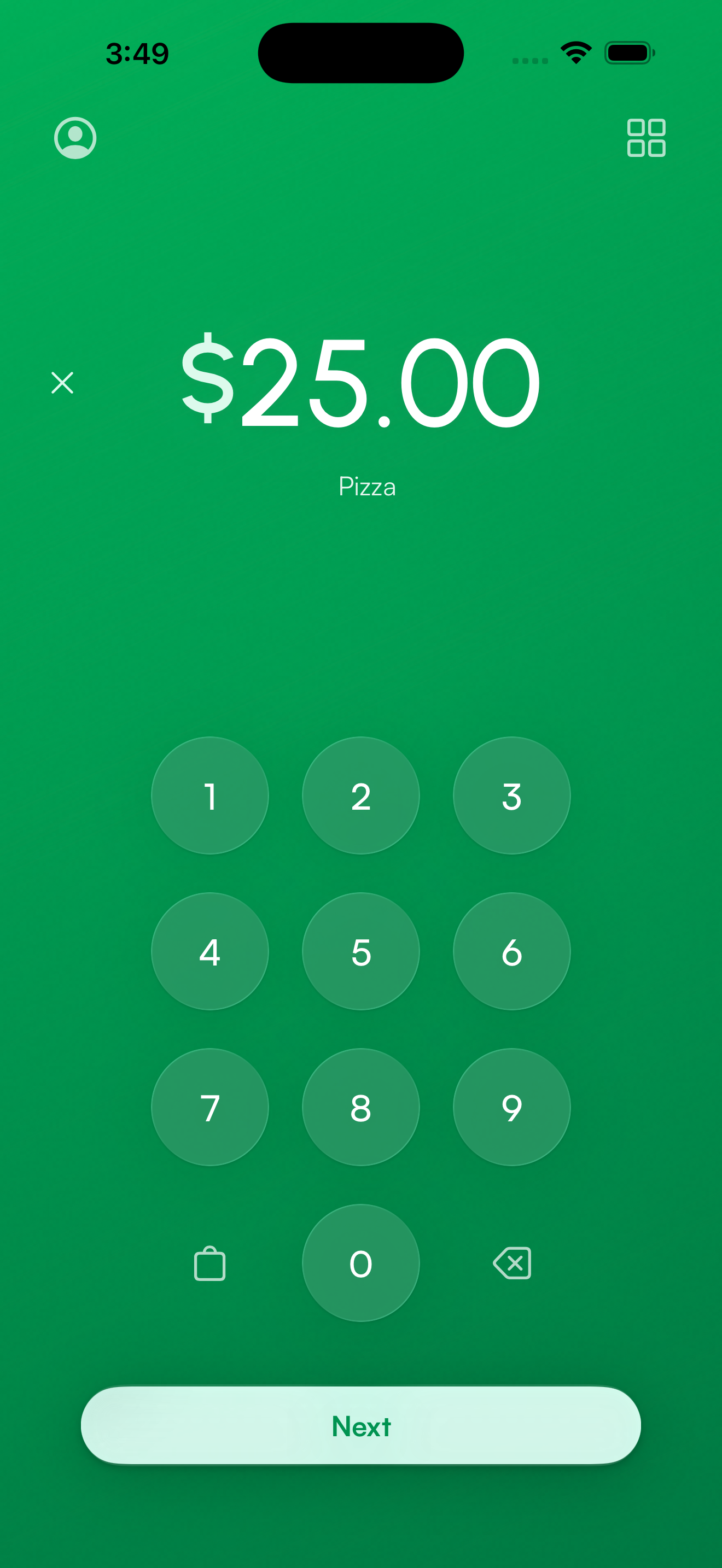

Stripe Terminal

Stripe Terminal Card Readers

Choose the right card reader for your business. All readers work seamlessly with Payment for Stripe and your existing Stripe account.

Choose your reader

Find the perfect card reader

From portable Bluetooth readers to all-in-one smart terminals, we support the full range of Stripe Terminal hardware.

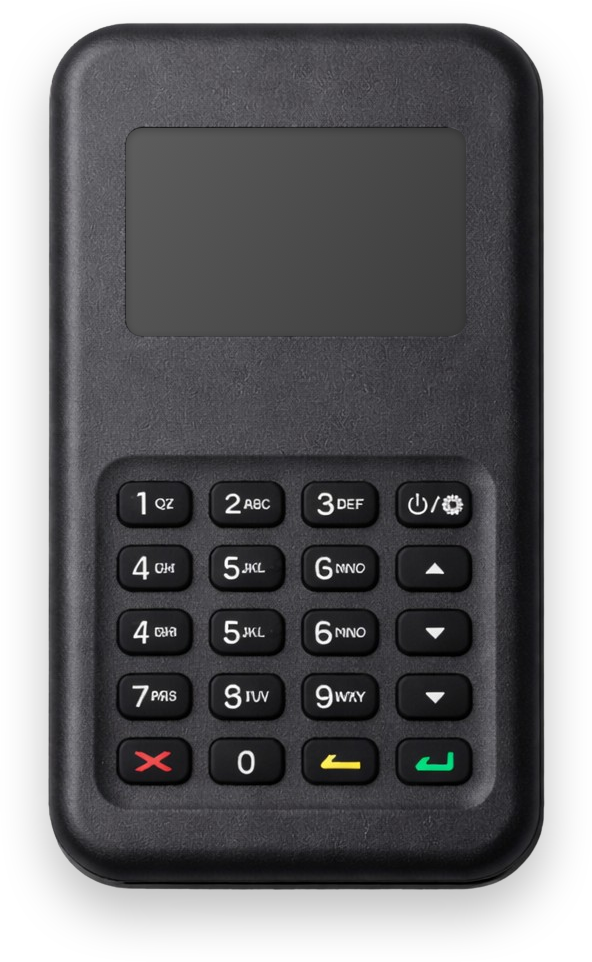

Quick comparison

| Reader | Price | Connectivity | Best For | Availability |

|---|---|---|---|---|

| Stripe Reader M2 | $59 | Bluetooth | Mobile businesses | US only |

| Stripe S700/S710 | $349 | WiFi / Cellular | Standalone terminal | International |

| WisePad 3 | CA$79 | Bluetooth | International merchants | Everywhere but US |

| WisePOS E | $249 | WiFi / Ethernet | Countertop use | International |

Benefits

Why use a card reader?

Card readers offer the lowest processing rates and most secure payment method for in-person transactions. Accept chip cards, contactless payments, and digital wallets with confidence.

Lower processing fees

In-person card transactions are charged at 2.7% + 5¢—lower than online rates of 2.9% + 30¢.

Chip & EMV security

Accept chip cards for enhanced security and fraud protection. Meet PCI compliance requirements.

Offline capability

Process payments even without internet. Transactions sync automatically when you reconnect.

Contactless payments

Accept Apple Pay, Google Pay, and contactless cards. Fast, secure tap-and-go payments.

Stripe processing rates

Card present

Card reader / Tap to Pay

2.7% + 5¢

Lowest rate

Card not present

Manual entry / Online

2.9% + 30¢

Standard rate

+ 1% app fee on charges created through Payment for Stripe. Stripe fees are set by Stripe and may vary by country.

Try Tap to Pay

Accept contactless payments using just your iPhone or Android phone. No card reader required—your device is the terminal. Same low 2.7% + 5¢ rate.

Learn about Tap to PayGetting started

How to get started

Order your card reader directly from Stripe, then connect it to Payment for Stripe.

Choose your reader

Pick the card reader that fits your business needs from the options above.

Order from Stripe

Purchase directly from your Stripe Dashboard. Readers ship directly to you.

Connect & accept payments

Pair with Payment for Stripe and start accepting in-person payments immediately.

Accept payments

in 60 seconds

Download the app, connect your Stripe account, and you're ready to accept your first payment. No hardware, no setup fees, no monthly costs.